With stimulus checks on the way, there will be tough financial decisions to make once received. Here are active steps you can take, along with things to consider to help you develop a solid spending plan.

1. Make a list of all expenses

Write out every single expense that you have, including essentials like food and utilities. Be sure to go through your checking and savings account history to make sure you don't have any “vampire” expenses, like monthly subscriptions that you may have forgotten about and no longer need.

2. Talk to all creditors and lenders

The CARES Act puts into effect two mortgage relief provisions: protection from foreclosure, and a right to forbearance (pausing or making partial payments) for those experiencing loss of income due to COVID-19. However, the provisions are not automatic and are only for federal loans, so you MUST talk to your lender.

If a creditor/lender offers you a payment plan or other relief, make sure you get it in writing and take note of the names and dates of the customer service representatives with whom you speak.

Thankfully, some utility companies have announced they won't cut off services if they aren't being paid. Be sure you know all of your utility and service providers' stance on this, so there are no surprises. You don't want to make any assumptions.

RELATED: Your lender might let you miss a few mortgage payments. Three questions you should ask first

3. Prioritize expenses

Expenses relating to food, shelter, and medicine should come first. This would include mortgage, rent, utilities, groceries, diapers, and medications. It also includes medical insurance premiums and homeowners/renter's insurance.

If you need childcare to work, that is another essential expense. Next in line are auto-related expenses, including transportation, gas, insurance premiums, and car payments.

Loans that are secured by collateral (for example, mortgages and auto loans) are generally considered more important than those without collateral, like consumer credit card debt. For example, if you don't pay your mortgage, a bank can foreclose on your property; if you don't pay your car loan, the bank can seize your car. While not paying your credit card bills will negatively affect your credit score, credit card companies will not come into your house and take your personal possessions.

Federal student loans are currently not accruing interest until September 30, 2020, and can be put into forbearance so that no payments are due. If you have a private or institutional loan, you will have to contact the lender for other options.

Remember, if you can afford the minimum payments on your credit cards, then make those payments. It will help to maintain your credit score.

Expenses for "elective" items, like gym memberships, streaming services, and other subscriptions, come last. Before simply canceling a contract, make sure to contact the vendor – canceling may come with a hefty penalty, but you may be able to temporarily "pause" the service.

4. Pay your debts in the order of priority

Now that you know all your expenses, have prioritized them, and know your payment options with creditors and lenders, it's time to make the payments in order of priority.

It's important to note that we are approaching tax season, so many expect to receive their tax refunds in the coming months. If you plan to receive a refund, you can apply the same process to that extra income.

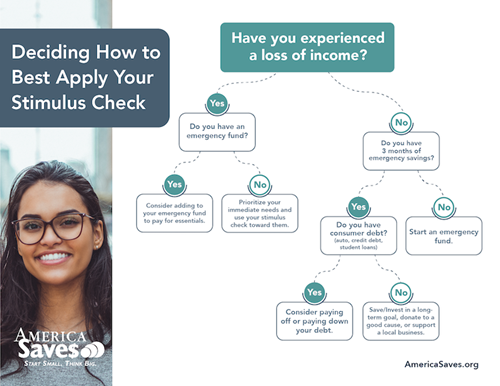

If you are still unsure or are overwhelmed with where to start, use our decision tree for guidance on what to do with your stimulus check and tax refund.

Then make a commitment to be more proactive with saving by taking the America Saves pledge. We'll be your savings accountability partner as you take a small step toward saving.

Download Decision Tree: PNG | PDF

Then make a commitment to be more proactive with saving by taking the America Saves pledge. We'll be your savings accountability partner as you take a small step toward saving.

If we feature you in our newsletter, you get $50.